It’s an exciting time for group benefits in Canada. That’s not a phrase you hear every day, but it’s one that’s coming up more and more often.

Terms like “digital health” and “disruption” are new words to the Canadian benefits vernacular. All of a sudden, it seems like a new digital health startup launches every day and incubators, accelerators and labs are popping up everywhere.

But what does it all mean for group insurance? What will these new services, startups, innovation labs and disruptors really do to change how plan sponsors and employees manage their health and insurance?

Read: Consultants seeking solutions amid disruption, competition

Over the past decade, health plans at all levels in Canada have become much better at managing costs. Employer health plans increasingly require proof of value before covering a new medical service or pharmaceutical product. The challenge, however, arises when the item under consideration is genuinely new and innovative. As difficult as it is to assess a new prescription drug, evaluating a service unlike anything currently offered can be nearly impossible. By definition, a service that has only existed for two years can’t have demonstrated a long-term return on investment. As a result, good ideas and new technologies face implementation delays.

So what do the new solutions look like and how can the industry ensure employers have access to them while still managing costs?

The new solutions come in many forms. They include:

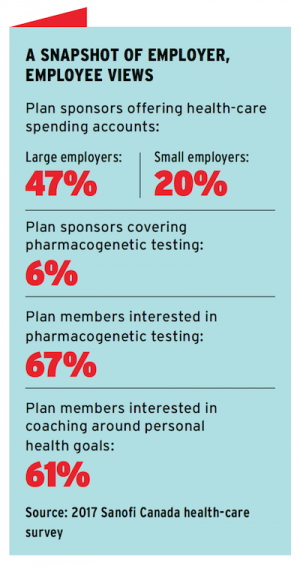

Pharmacogenetics: Personalized medicine is one of the great developments in health care. It has begun to arrive, and pharmacogenetics represent one of the first ways in which we see personalized medicine becoming available to group insurance plans.

Read: Pharmacogenetic testing a growing area as pilot projects, research get underway

Telemedicine: Access to prompt medical advice is one of the most commonly cited shortcomings of the Canadian health-care system. Due to an apparent gap in the definitions under the Canada Health Act, provincial plans generally don’t cover remote or virtual access to physicians. There are now multiple providers of the service on a per-visit or annual subscription basis. For employers, the potential time savings to their employees are significant. Is covering an on-demand video call with a doctor or nurse not more cost-effective than an employee taking time off work to wait at a clinic or in an emergency room?

Pharmacists: The idea of pharmacists doing more than simply dispensing pills by providing value-added services, such as coaching for patients with chronic disease, has been a solution waiting to happen. After years of discussion, the idea has yet to take hold. Why is that? Pharmacists will offer the services if employer benefits plans provide reimbursement. Employer benefits plans, in turn, are open to covering those services once there’s a proven track record of added value.

Read: Pharmacists’ role evolving to help plans manage costs

Gene therapy: The ability to alter someone’s genes to cure a disease (or eliminate the risk of developing one) will soon be a reality. How will benefits plans handle a genetic treatment for a disease, such as cancer, that someone is at risk for but doesn’t yet suffer from?

Health coaching and navigation: Unfortunately, most Canadians don’t get enough time with public health professionals either to stay healthy or get help, when they fall sick, in navigating the system efficiently. As a result, wellness, coaching and navigation alternatives are growing fast, often using technology to personalize and automate the services and thus drive down the cost and improve employee health at the same time.

Health coaching and navigation: Unfortunately, most Canadians don’t get enough time with public health professionals either to stay healthy or get help, when they fall sick, in navigating the system efficiently. As a result, wellness, coaching and navigation alternatives are growing fast, often using technology to personalize and automate the services and thus drive down the cost and improve employee health at the same time.

Virtual care: In-person care has historically been the default way to see a health practitioner. But what if, instead of seeing a psychologist in person for $150 per hour, plan members could treat their mental-health issue by using a cognitive behavioural therapy app on their phone? Is that not worth paying the $60 annual subscription to access it? Despite the potential, most benefits plans haven’t developed a framework to assess the value of or reimburse virtual care.

Read: A look at video health-care visits as an option for plan sponsors

Health-care spending accounts: New entrants into the group insurance market have sparked a growing debate recently about the role health-care spending accounts could and should play in benefits plans. Given the predictability of many kinds of expenses covered (such as paramedical services, dental recall exams and vision care), the concept of a health-care spending account as the primary source of coverage, with adequate real insurance for catastrophic expenses, is a valid structure to consider.

Medical marijuana: For a variety of reasons, information on both the therapeutic value and cost effectiveness of marijuana in a benefits plan is often still anecdotal. Would a plan that covers medical marijuana see an increase or a decrease in overall costs? For whom and under what circumstances could it be a benefit that outweighs the cost?

Read: What’s the impact of medical marijuana on patients, drug plans?

2018’s greatest idea: One of the great joys of the speed of technology is there’s almost certain to be a number of new ideas added to the list of innovations in the coming months. That means that considering new solutions needs to become part of the ongoing review of any benefits plan.

How can plan sponsors integrate new solutions?

The biggest challenge plan sponsors face in terms of adopting a new solution is the default position generally requires that any additional cost must demonstrate value to employees and a proven return on investment.

Of course, the idea of covering items only with a proven return is a healthy one. But it’s important to view the idea of return, in this context, holistically. Certainly, financial return is one element, but increased employee satisfaction, engagement and productivity are also important.

Looking at every new service that way puts the decision in isolation and takes it out of the context of the broader plan. The standard of proven return is also one that many of the services covered under benefits plans today wouldn’t be able to meet.

If that’s the case, is it time to step back and take another look at what plans will and won’t cover?

Read: Pitney Bowes focuses on prevention in benefits redesign

When plan sponsors are willing to look critically at which services they should cover under a benefits plan, it can sometimes become apparent that the current design doesn’t always prioritize the most effective elements. Could one or more of the examples below better balance cost and value?

- Covering low-cost services, such as paramedical, vision and basic dental care, through a health-care spending account.

- Reducing massage therapy coverage to 50 per cent co-insurance, while adding benefits for virtual care and telemedicine also at that level.

- Expanding the concept of prior authorization to include access to health coaching, health navigation or pharmacogenetic testing for employees with certain health needs.

- Facilitating employee access to new services by offering them on an employer-negotiated, discounted basis.

When looking at whether to add a new plan feature, employers don’t need to offer it at 100 per cent coverage or to all employees and under all circumstances. Being creative in merging new solutions with established ones will differentiate those plan sponsors that are willing to embrace change and use technology to engage employees in their health.

Tim Clarke is president of TC Health Consulting. His clients include some of the new entrants

and disruptors in the health-care industry. This is the first of two articles about emerging innovations in health and group insurance.