“For those investors that are comfortable with a higher-thancore risk profile, we are able to create and leverage this same approach with an even greater return potential.SUNIL SHAH, CFA

HEAD OF CANADIAN FIXED INCOME, AVIVA INVESTORS

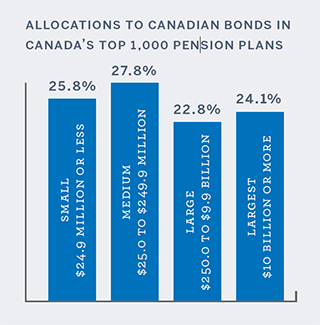

CANADIAN FIXED-INCOME PERFORMANCE MATTERS

Canada’s top 1,000 pension plans invest an average of 24.1% of their assets in Canadian bonds, making the impact of a potential incremental return advantage significant for plan sponsors and their members.

Source: The data in this article is based on the top 1,000 pension plans, collected from March 1, 2017 to September 30, 2017 (and previous five years), with an accounting year-end date of December 31, 2016, through the Canadian Institutional Investment Network (CIIN) database.

Important information:

Except where stated as otherwise, the source of all information is Aviva Investors Canada, Inc. (“AIC”) as

of October 31, 2017. Unless stated otherwise any views, opinions and future returns expressed are those of

Aviva Investors and based on Aviva Investors internal forecasts. They should not be viewed as indicating any

guarantee of return from an investment managed by Aviva Investors nor as advice of any nature. The value

of an investment and any income from it may go down as well as up and the investor may not get back the

original amount invested. Past performance is not a guide to future returns.

AIC is located in Toronto and is based within the North American region of the global organization of

affiliated asset management businesses operating under the Aviva Investors name. AIC is registered with the

Ontario Securities Commission (“OSC”) as a Portfolio Manager, and an Exempt Market Dealer.

Aviva Investors is a global asset management firm comprised of a group of affiliated companies, each of which

is regulated in the jurisdiction in which it operates. Each Aviva Investors affiliate is a subsidiary of Aviva plc,

a publically traded multi-national financial services company headquartered in the United Kingdom (UK).

There are risks associated with all investments and those risks may be higher for strategies investing in

alternative, derivatives and small cap asset classes.