BRIJ KHURANA

MULTI-ASSET PORTFOLIO MANAGER WELLINGTON MANAGEMENT

HOW SHOULD CANADIAN INVESTORS THINK ABOUT THE RISK OF ALLOCATING AWAY FROM CANADIAN MARKETS?

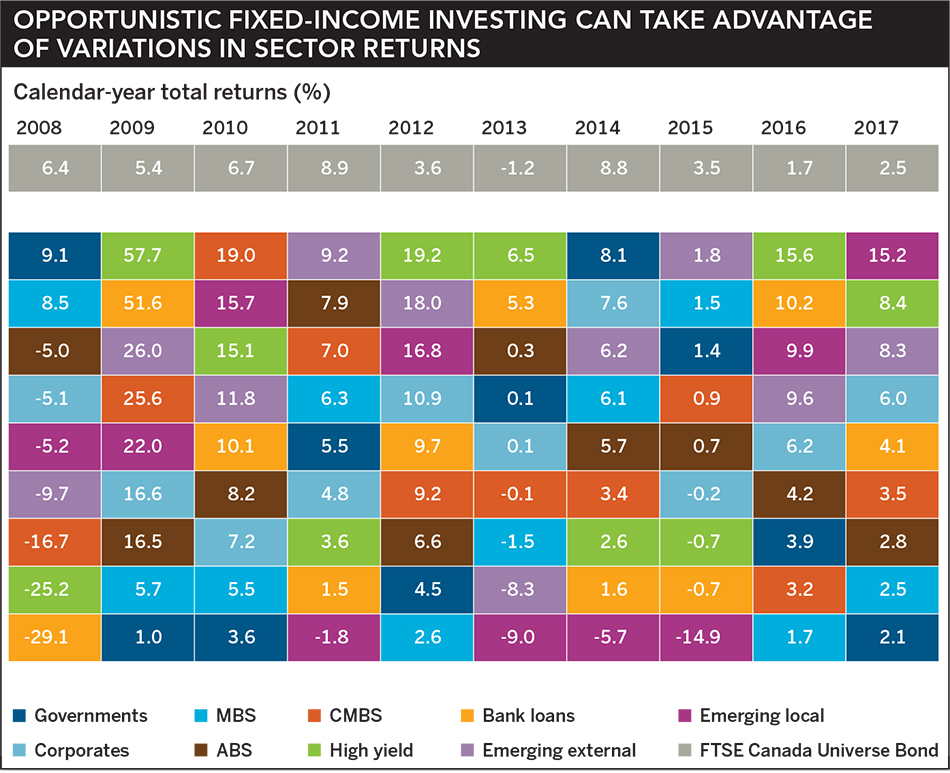

I think the biggest risk Canadian investors should consider is concentration risk. We are now exiting a 10-year period of unprecedented synchronized global monetary and fiscal stimulus that has dampened the volatility of riskier, higher-yielding sectors of the global fixed-income markets. As this unprecedented level of liquidity is removed and central bank policy diverges, we expect volatility in higher-yielding sectors to return to their pre-crisis averages. We strive to diversify risk by not concentrating on any single sector or risk factor and by pursuing a volatility profile that is in line with relevant core fixed income indices.

WHAT CAN INSTITUTIONAL INVESTORS GAIN BY INCORPORATING OPPORTUNISTIC INVESTING INTO THEIR FIXED INCOME ALLOCATION?

Opportunistic allocations can access non-Canadian markets that offer more attractive yields and return potential, while providing significant diversification by region, country, and sector and security type. Moreover, well designed opportunistic strategies can be highly dynamic, allowing for timely allocation, which many institutional investors would be challenged to replicate given the internal review process required to make new standalone allocations.

Learn more:

www.wellington.com/Canada

This material and/or its contents are current at the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the express written consent of Wellington Management. This material is not intended to constitute investment advice or an offer to sell, or the solicitation of an offer to purchase shares or other securities. Investors should always obtain and read an up-to-date investment services description or prospectus before deciding whether to appoint an investment manager or to invest in a fund. Any views expressed herein are those of the author(s), are based on available information, and are subject to change without notice. Individual portfolio management teams may hold different views and may make different investment decisions for different clients.

All investing involves risk. Principal risk considerations for investing in opportunistic fixed income strategies include: below investment grade, credit, hedging, short selling, capital, currency, interest rate, derivatives, concentration, emerging markets, leveraging and manager.