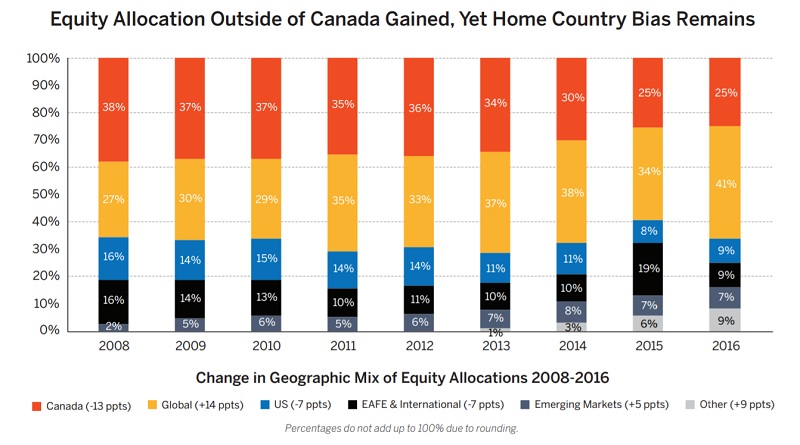

Moving wealth outside a sector they rely heavily on may help balance what Norway can provide for its citizens long term. I recommend investors consider diversifying further outside Canada, a stock market that is both relatively small in global context and heavily concentrated in the resource and financial services sectors.

Looking at the impact over 10 years ending October 31, 2017, a portfolio of 10% TSX stocks and 90% global stocks would have had the same volatility as a portfolio of 55% TSX stocks and 45% global stocks – yet the first portfolio would have returned nearly 200 basis points more for investors. So, reducing home country bias can improve returns with the same level of risk.

HOW CAN A GLOBAL APPROACH TO INVESTING CONTINUE TO ADD VALUE IN AN ENVIRONMENT OF RISING POPULISM AND DEGLOBALIZATION?

We think a global approach is increasingly relevant because investors can rely less on multinational companies for global exposure. Furthermore, regionalization will create greater dispersion among companies in terms of returns, and a global approach can free investors from the political luck or misfortune of their postal code. Ultimately, a global, systematic and disciplined approach to investing can create an all-weather portfolio no matter where the political winds blow.

HOW DOES YOUR TEAM MANAGE MARKET VOLATILITY RESULTING FROM IMPROBABLE POLITICAL EVENTS SUCH AS THE RESULTS OF THE BREXIT REFERENDUM AND THE U.S. ELECTION?

Politics are definitely becoming less predictable, and so is the market reaction. For example, Trump’s election was a low probability event that was supposed to send global markets into a downward spiral, but the morning after, the markets rallied quite significantly. Similarly, with Brexit, the rout lasted only a few days. We manage this unpredictability through portfolio construction, where country allocation provides a framework for remaining disciplined and invested across most attractive geographies and markets. We focus on diversifying styles and looking for companies that are strong generators of economic value-add and provide good downside capture. We also look at monetary policy, which we believe is more predictable than politics, and build in natural hedges to account for the fact that we may be wrong in our base case.

WHAT ARE THE ATTRIBUTES OF A SUCCESSFUL COUNTRY ALLOCATION FRAMEWORK?

The most important attribute of a country allocation framework is to create a collection of independent factors that give you the greatest power to deliver alpha. Ours is a multifactor model, with various factors classified into valuation, sentiment and risk categories – valuation being the most important. We also work hard to make sure these factors are not correlated with each other. We focus more on market signals – observed prices and valuation multiples – than on macroeconomic factors. Even if you had perfect foresight of macro data, you’d have very limited ability to deliver alpha in global markets. Macroeconomic variables, including GDP, explain very little of equity market performance.

HOW DO YOU MITIGATE RISK FOR PENSION PLANS WITH GLOBAL EQUITY EXPOSURE?

The conversation around risk has evolved. We used to talk about volatility and tracking error, but the ultimate liability of a pension fund is to meet its obligations. That is an absolute hurdle, not a relative hurdle, and it is tougher in a low return environment. To us, risk means absolute loss of capital and/or sustained relative underperformance. We manage risk in two ways. One, we favour companies that generate high returns internally because we believe that will translate into high returns for their equities. Two, we construct portfolios of idiosyncratic and uncorrelated alpha streams. Idiosyncratic means things that are specific to that security and unrelated to broader market movements, and uncorrelated means things that move that particular security are different from things that move other securities. For example, a Brazilian iron ore company and a Singaporean real estate development company may be in different geographies and sectors, but both are driven by China’s housing development. Making sure we don’t have these correlated exposures in our portfolio is extremely important, unless we are rewarded handsomely to take these risks. Ultimately, through security selection and portfolio construction, we aim to deliver to our clients a collection of equities that helps pension funds meet their absolute return obligations.