SARAH DONAHUE

MANAGING DIRECTOR OF CONSULTANT RELATIONS,

MFS INVESTMENT MANAGEMENT

NADIA SAVVA

MANAGING DIRECTOR OF PLATFORMS AND SUBADVISORY,

MFS INVESTMENT MANAGEMENT

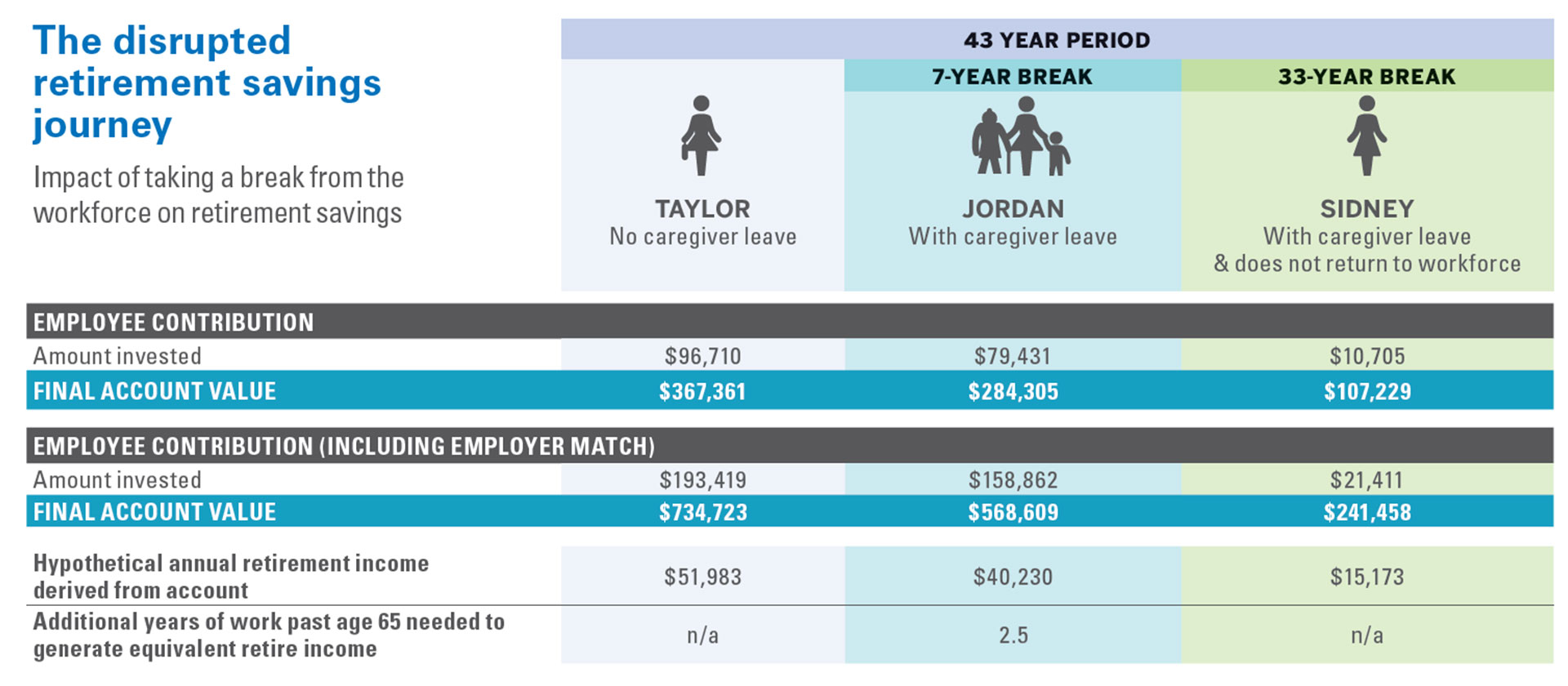

An article from The New York Times highlighted the 10-year baby window that’s the key to the pay gap. It uses U.S. census data and shows women who take a gap before the age of 25 and after the age of 35 are actually in a pretty good position to narrow the pay gap with their male counterparts. But the ages between 25 to 35 are peak retirement saving years—and this is when women tend to take time off to start families. That’s something I’ve experienced on a personal level. I didn’t think waiting to have kids was going to increase my chance of narrowing the retirement gap, but I knew if I could get to a certain level in my career it wouldn’t be as hard to catch up. Unfortunately, for me and many women, when you wait too long to have kids, you can experience fertility issues. I was one of them—and I ended up having to go through fertility treatments to have my child. There can be a career cost to parenthood; women have to consider not only the tradeoff s of their career and starting a family, but also their biological clocks. It’s an additional layer of stress women tend to experience.

WHAT CAN EMPLOYERS DO TO ENSURE WOMEN ARE ON TRACK TO MEET THEIR RETIREMENT INCOME GOALS?

DONAHUE: From a plan design and advice perspective it makes sense to consider how best to communicate with plan members—both men and women—because one size does not fit all. Special attention needs to be paid to the plan design to ensure it doesn’t worsen gender inequality in retirement. Some of our suggestions would be providing fi nancial incentives for women to join and save within plans. We also know auto-enrolment, re-enrolment and auto-escalation features can have material impacts on improving retirement savings. Plan sponsors can also tailor their communications to women in order to raise the importance of savings and where women might possibly contribute to their plans however and whenever they can.

HOW SHOULD THIS INFLUENCE DC PLAN SPONSORS’ TARGET-DATE FUND LINEUP?

DONAHUE: Compared to men, women are found to be more risk averse and have lower levels of financial literacy overall— and this definitely influences their attitude toward savings. Previous studies have shown how women might invest in more conservative solutions than what their actual risk to improve investment returns on women’s retirement savings by implementing non-conservative default investment options. We advocate for a suite of targetdate funds to be the default solution for CAP plans, which is becoming more prevalent. It has definitely helped women assume similar levels of risk and return in comparison to men.

Based on our annual plan member survey data, we’re seeing an opportunity to educate not only women on the benefits of target-date funds, but men as well. Thirty-two per cent of plan members who aren’t using target-date funds said they don’t understand the benefits.

But a target-date fund is hugely beneficial and easy to use for busy women—they can just set it and forget it. Should a plan member not be engaged, it’s better for them to be invested in a target-date fund that’s allocating responsibly for them. There’s a benefit to inertia. In our survey we found that 55 per cent of men took no action when it came to their retirement savings during COVID, as opposed to 70 per cent of women. There’s power in leaving that money invested in a strong retirement solution.

WHAT KIND OF TARGET-DATE FUND GLIDE PATHS MAKE THE MOST SENSE FOR THESE EMPLOYEES?

SAVVA: The biggest difference among the target-date funds out there is the glide path. In particular, women may want to consider target-date fund suites with a curve that’s a bit steeper in the earlier years so they have the opportunity to catch up if they take a gap. Small adjustments can be made to get women back on track after missing years in the workforce, such as determining the extra contributions needed to move in the right direction or what target-date vintage is right for them.

DONAHUE: Plan sponsors should offer plan members an intuitive glide path that balances capital accumulation early on and downside protection in retirement. We believe one that starts off more aggressive will benefit women, with the goal of emphasizing wealth accumulation and taking advantage of wealth compounding over time. Closer to retirement, a glide path should be focused on capital preservation, with a more conservative allocation.