Where does your interest in financial markets come from, and how did you come to join Fidelity?

I grew up in the Eastern Townships, in a small rural town in Quebec, far removed from the world of finance. In the late 1990s, during the dot-com bubble, I witnessed the explosive rise of technology stocks, and then their fall. I wondered how a sector that everyone was talking about and that had unanimous support could have collapsed in such a short period of time, and it piqued my interest in understanding how markets worked.

When I was studying at HEC Montréal, I got very involved in the Student Investment Fund, the FPHEC. I probably spent more time doing business analysis for that fund than studying for my courses! I set myself the challenge of getting hired by a major U.S. asset manager. My English wasn’t very good at the time, however, so I felt I had to stand out by working even harder than everyone else.

Because the competition to join the industry was so intense, I decided to go to Queen’s University for a master’s degree after completing my bachelor’s degree at HEC. Then I had the good fortune and privilege of starting my career at Fidelity in Boston. For my first eight years, I was part of the Canadian group and covered a wide range of sectors in Canada. Our team kept expanding, and in 2009, it was repatriated to Toronto. So I came back home to Canada, but my interest in the global market was growing. In 2013, after a decade of hard work, I was entrusted with the Fidelity Global Concentrated Equity strategy, which I still manage today.

I am still very proud of this accomplishment. Coming from a small corner of Quebec, it would have been easy to be intimidated at the start of my career when all my colleagues were graduates of major American universities. But I think if you’re really motivated and put the effort in, there’s room to set yourself apart, even in a very competitive world.

You’re known for your contrarian style of investing. Can you tell us more about this approach?

As a general rule, I think markets are relatively efficient, but there is a tendency for market players to exaggerate the fundamentals that are currently being observed. This creates tremendous momentum for some stocks, and as quarters and years pass, often leads to overrepresentation in assessing the impact of what is happening today.

For my part, I try to focus on the portions of the market where there has been an overreaction to certain negative events. My approach is to take advantage of a longer time horizon by assessing businesses not on today’s fundamentals but on long-term standardized fundamentals. I don’t look at the profitability outlook for next year; I look at the next 15 years.

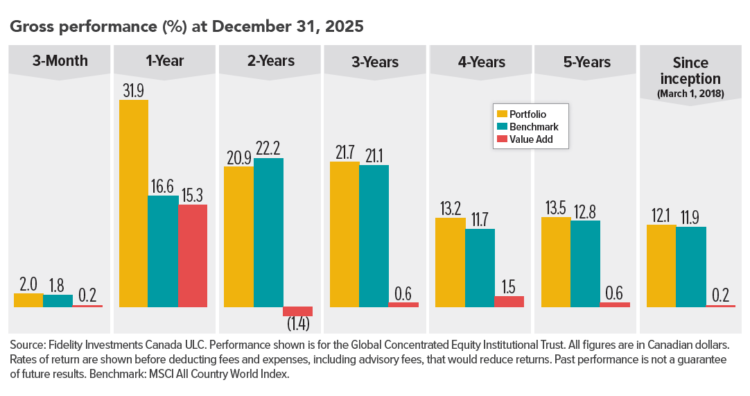

Generally speaking, I would say that I invest in portions of the market that are at or near the bottom of their cycle. I’m willing to do that a little earlier than most investors, and I’m patient as I wait for things to normalize. However, as part of my analysis process, I make sure that I select businesses that will be able to get through a more difficult situation rather than falling victim to it. In 2025, we outperformed our benchmark by 15% through this approach.

How does this strategy translate concretely into your portfolio management?

I spend a lot of time looking at where extremes might have been created in terms of overreaction. Over the past decade, all eyes have been on the overperformance of the United States, led by the technology sector. We see this today, for example, with extremely high capital expenditures (CapEx) in the data centre sector, in line with the growth of artificial intelligence. I think there’s a real possibility that we’re exaggerating the future profitability of this sector.

What I see is that in recent years, it has become more difficult to find companies that appear to be undervalued in a variety of sectors of the U.S. market. I think this trend is accompanied by a perhaps exaggerated pessimistic outlook in other parts of the market, particularly in Europe and China, but also in many small-cap and mid-cap securities.

In the current political environment, do you feel that Canadian investors are seeking to reduce their exposure to U.S. assets?

There’s clearly more interest in international markets outside the United States, and that’s not limited to Canada—I think it’s a global phenomenon.

In 2024, when we compared two very similar multinationals competing internationally, one incorporated in the United States, and the other elsewhere in the world, we found considerable gaps in evaluation. Yet, there were few legitimate long-term reasons for a valuation premium that was so much higher among U.S. companies.

In the last 18 months, since Donald Trump has returned to the White House, we’ve seen the gap narrow, but I think there are still opportunities outside of the United States. I think we’re potentially nearing a peak of the cycle in the United States, and at the same time, approaching the low point of the cycle in the rest of the world.

Contrarian investing often requires going against dominant market discourse. How do you maintain your conviction when the general feeling isn’t in your favour?

Obviously, it’s not always easy. If that were the case, the contrarian approach would be more widespread, which would likely destroy its potential. It’s hard to buy parts of the market that aren’t performing that well; it goes against everything we hear in the media. There’s also a credibility risk to this approach, because if we make a mistake, everyone will say that we should have known better.

I think there are a growing number of market participants who have a shorter and shorter time horizon based on high-frequency data. There is a very big momentum bias at the moment, so taking the opposite approach could turn out to be really beneficial when we see a change of leadership in the market.

Could you share an opportunity you see in the markets in the future?

After many years of technology leading the market, I think we could see a resurgence of what I call the “old economy.” I include here the discretionary spending sector, the automotive industry, transportation, building materials, chemicals, mining, and so on. Those sectors have fairly low assessments and expectations, and I think they have the potential to rebound.

I believe that the next decade could also bring a more intense level of competition to several markets, particularly caused by the entry of Chinese companies into sectors and regions historically dominated by large western multinationals. This will create multiple risks, but also some opportunities that can benefit from these major structural changes.

Issued by Fidelity Investments Canada ULC (“FIC”).

Unless otherwise stated, all views expressed are those of Fidelity International, which acts as a subadvisor in respect of certain FIC institutional investment products or mandates.

This document is provided for information purposes only and is intended only for the person or entity to which it is sent. It must not be reproduced or circulated to any other party without the prior permission of Fidelity.

This document does not constitute a distribution, an offer or solicitation to engage the investment management services of Fidelity, or an offer to buy or sell or the solicitation of any offer to buy or sell any securities in any jurisdiction or country where such distribution or offer is not authorized or would be contrary to local laws or regulations.

These materials may contain statements that are “forward-looking statements,” which are based on certain assumptions of future events. Forward-looking statements are based on information available on the date hereof, and Fidelity Investments Canada ULC (“FIC”) does not assume any duty to update any forward-looking statement. Actual events may differ from those assumed by FIC when developing forward-looking statements. There can be no assurance that forward-looking statements, including any projected returns, will materialize or that actual market conditions and/or performance results will not be materially different or worse than those presented. Past performance is not a reliable indicator of future results.

©2026 Fidelity Investments Canada ULC.

All rights reserved.