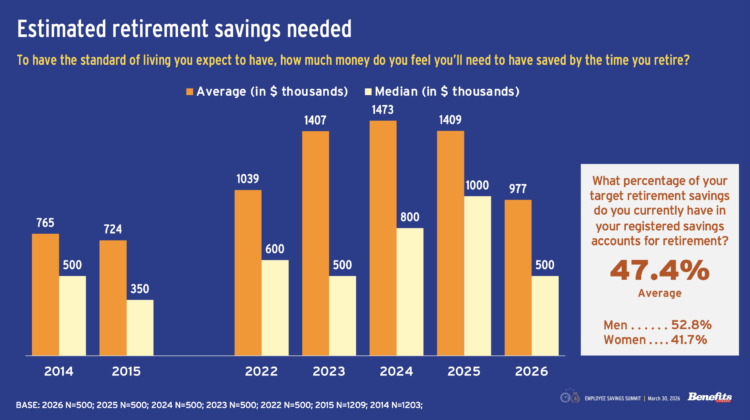

Canadian plan members reported a significant drop in the amount they believe they need to retire — from roughly $1.4 million in 2023, 2024 and 2025 to $976,835 in 2026, according to Benefits Canada’s 2026 Employee Savings Survey.

The survey, which polled 500 Canadian savings plan members, also found younger and middle-aged respondents reported requiring just over $1 million on average, while those aged 55 and older were more likely to cite a much lower amount.

“The mean dropped by 31 per cent, but the median dropped by 50 per cent,” said Jimmy Carbonneau, national director of group retirement, group insurance and group annuity plans advisor at AGA Benefit Solutions, during a webinar discussing the survey results.

Read: Pension Awareness Day 2026: FSRA highlighting plan member education, retirement readiness

Strictly looking at the numbers, these results look drastic, he said, but if plan members’ finances have been well-managed — with debt under control and their lifestyles adjusted — maybe having less money won’t make them any less happy.

The fundamental question is whether plan members are recalibrating their expectations or giving up, added Carbonneau. “If it’s all well-intended and calculated, this is good. People are recalibrating. If not, then we have an issue.”

This year, the survey asked plan members how much of their targeted retirement savings is currently in their registered savings account. The response across all respondents was 47.4 per cent, but it was slightly higher for men (53 per cent) and slightly lower for women (42 per cent).

Tawnya Duxbury, assistant vice-president of products and solutions for workplace retirement at Canada Life, noted women typically have about 55 per cent of the assets that men hold in their retirement savings and it hasn’t changed significantly in the last 10 years. This is likely a reflection of several factors, she added, including the gender pay gap, ineligibility for part-time workers and the higher likelihood of women taking career breaks for caregiving responsibilities.

Read: Women lag men in use of workplace retirement savings plans: report

Another factor that’s often overlooked is women’s investment behaviour. “Women tend to be more conservative in their investments. Even in a target-risk fund, males are picking the more aggressive fund, . . . while women will generally pick more conservative or balanced investments, so they don’t get the same compounding.”

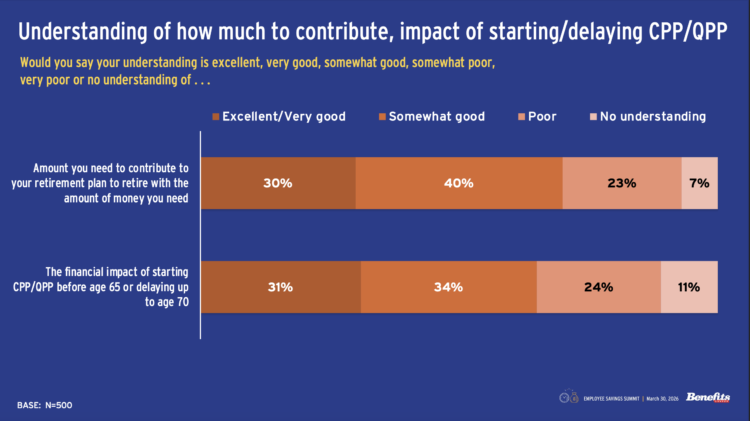

The survey also asked plan members about their level of knowledge around government sources, such as the Canada/Quebec Pension Plan and old-age security. It found respondents said they expect 41 per cent of their retirement income to come from government sources — nearly double the 22.3 per cent recorded when the question was last asked in 2021.

Dean Newell, vice-president of Actuarial Solutions Inc., said the CPP and QPP play a critical role for defined contribution plan members. “For members with defined contribution savings, the CPP isn’t just another income source; it’s an inflation-indexed guaranteed lifetime income.

Read: Helping employees understand the benefits of delaying CPP/QPP

“It’s encouraging to see a large percentage of plan members report having a good understanding of the CPP,” he added. “However, it’s important to look closely at what that understanding represents. I suspect most members understand the basics — that benefits can start between age 60 and 70, that starting early reduces payments and delaying increases them — but what’s likely missing is a true appreciation of how large and permanent those adjustments are and how CPP timing interacts with their DC account balance.”

Sharing a plan sponsor perspective, Angela Rawal, principal of pension programs at Export Development Canada, said the organization consistently directs employees to the federal government’s tools for estimates on their entitlements because it helps to ensure people are working with accurate data and making informed decisions.

“I know a lot of plan sponsors put estimates of CPP entitlements on their annual statements and those typically rely on the average or maximum CPP benefits paid out. But this may not reflect these individual employees’ realities.”

More coverage of the 2026 Employee Savings Summit will be rolled out on the website in the coming days.