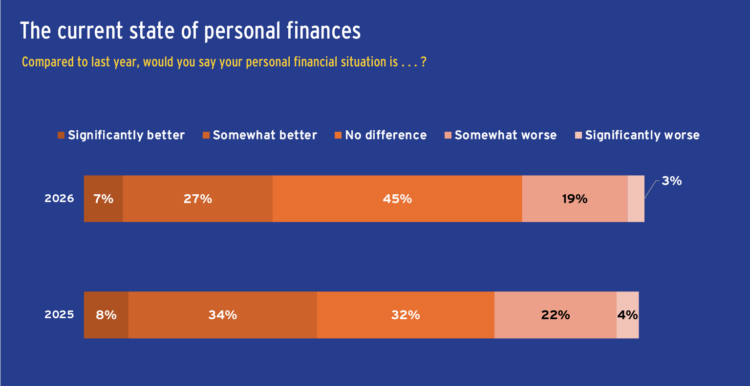

While the percentage of plan members who describe their personal financial situation as significantly or somewhat better than last year decreased from 42 per cent in 2025 to 34 per cent, the percentage that describe it as significantly worse or somewhat worse has also dropped, from 26 per cent last year to 22 per cent, according to Benefits Canada’s 2026 Employee Savings Survey.

During a webinar discussing the survey’s results, Jimmy Carbonneau, national director of group retirement, group insurance and group annuity plans advisor at AGA Benefit Solutions, said these findings are indicative of an E-shaped economy — in which higher-income employees continue spending and lower-income workers scale back their consumption — and likened the results to a car’s check-engine light. “I’m not saying the car is run down or is beyond repair, but some parts may need attention or an upgrade.”

Read: How employers can improve women’s financial security, close gender pension gap

For the first time, the survey, which polled 500 plan members across Canada in January 2026, asked how the cost of living has impacted their personal financial situations, with a majority (61 per cent) saying somewhat or very negatively. Those with household incomes between $60,000 and $99,000 were the most likely to agree with this statement, at 76 per cent, followed by those in the highest income bracket (more than $150,000) at 63 per cent. Interestingly, respondents with household incomes lower than $60,000 were the least likely to agree, at 46 per cent.

Also speaking during the webinar, Tawnya Duxbury, assistant vice-president of products and solutions for workplace retirement at the Canada Life Assurance Co., noted middle- and high-income households are feeling the pinch as a result of reduced discretionary income.

“They’re dissatisfied they’re not saving at the same rate, they’re not able to do renovations like they expected [or] maybe they have to cut back on travel. No [middle-income or higher] household is immune to the financial situation that’s going on right now.”

Read: UAP supporting financial well-being, retirement readiness with enhanced toolkit

For several years, the survey has asked respondents to rank their top financial priorities, with paying for day-to-day expenses consistently taking the top spot. This year, saving for retirement was up five percentage points — from 42 per cent to 47 per cent — and creating an emergency fund was up three percentage points — from 36 per cent to 39 per cent. Those in the top income bracket were the most likely to rank saving for retirement as their top priority.

During the webinar, Dean Newell, vice-president of Actuarial Solutions Inc., cited multiple reasons for plan members’ prioritization of emergency and retirement savings, such as recent economic shocks and a broader cultural shift towards financial preparedness. “Rather than spending freely during the good times, people are thinking more defensively [and] preparing for the possibility that conditions might worsen in the near future.”

Export Development Canada provides employees with several financial planning tools and resources through its employee assistance program and its record keeper, said Angela Rawal, the organization’s principal of pension programs. The organization’s savings plans include a defined contribution pension plan that requires an employee contribution of between four and six per cent, which is matched by the employer by a minimum of 125 per cent up to 200 per cent.

“We just want to make sure employees have access to the information and the support that they need to help them feel more comfortable. . . . Employees who spend less time focusing on the stresses of their financial situation will be more productive as well.”

More coverage of the 2026 Employee Savings Summit will be rolled out on the website in the coming days.