Since the financial crisis, the Pension Plan for the Employees of Concordia University has transformed the way it approaches investments by introducing its first funding policy and revamping its investment policy.

Historically, the plan had a 60/40 asset mix and its board of directors was completely focused on the asset side of the equation, says Marc Gauthier, the university’s treasurer and chief investment officer. In 2007, when he took over responsibility for the plan, he noticed its investments were heavily exposed to financial markets and vulnerable to major drawdowns. At the same time, the plan was governed by a 12-member board that was doing all the work.

Read: A primer on reviewing statements of investment policies and procedures

“They had no supporting management structure to recommend anything to them,” says Gauthier. “They would essentially recommend and approve their own recommendations and they had no sub-committee dedicated for investments.”

The board met four times a year and was more backwards-looking, focused on reviewing portfolio managers, he adds. Gauthier wanted to address the plan’s risks head on. “My DNA is risk management.”

His first instinct was to take on an enterprise risk management assessment; however, he says when he suggested the idea to the board, it wasn’t that interested and thought it would be a make-work project.

Getting to know

Marc Gauthier

Job title: Treasurer and chief investment officer

Joined the Concordia University: 1990, but took over responsibility for the pension plan in 2007

What keeps him up at night: Ensuring he’s prepared for every potential situation

Outside of the office he can be found: Working out and spending time with his family

But then the financial crisis arrived. Concordia’s plan dropped from over 100 funded on a going-concern basis to 74 per cent funded. “Now, they obviously couldn’t refuse to do the enterprise risk management assessment,” says Gauthier.

From a fiduciary perspective, he also knew that once a plan’s risk is identified as over its tolerance level, it would have to be addressed by the board. “That framework allowed me to provide a roadmap to ensure that action would be taken.”

The action began with the introduction of a funding policy. “Essentially, what came out of that process of developing a funding policy is that we defined that the objective [is] to have a stable and sustainable cost over the short, mid and long term. And, in order to do so, the investment policy was directed to be designed in a way that would minimize the absolute loss of capital, while still having the ability to meet the investment target, which is the discount rate of the plan.”

Read: Administrators will need to revisit governance policies under Ontario’s latest pension changes

Once the funding policy set the direction, the plan reviewed and redesigned its investment policy. “I must have invited over 15 to 20 portfolio managers to educate the committee on the . . . different strategies outside of the pure 100 per cent [benchmark-oriented strategy] that the plan used to have and also [on] the notion of risk budgeting,” says Gauthier.

Concordia’s plan opted to move to an absolute return-driven approach to portfolio construction because it aligned with the liabilities’ absolute-driven behaviour, he adds.

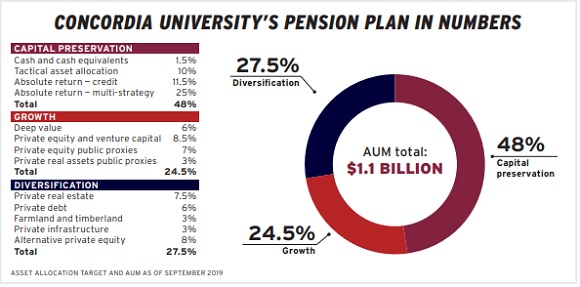

The new approach has three categories: capital preservation, growth and diversification. The capital preservation category is defensive first, but can be risk-on in proper conditions. The growth category focuses on specialization, concentration and high-conviction investments. And the diversification category is disconnected from capital markets. Real estate, for example, could fit into any of these categories.

“It allows it to be a lot more flexible, not related to constraints [of] a particular asset strategy or program, as long as it fits within the category and the allocation within the range,” says Gauthier.

During the change process, the board also brought in a new governance structure. It set up a specialized sub-committee, dedicated to investments, that meets monthly. And it’s more strategic about how it spends its time, covering education, discussion, strategic reporting and administration.

Read: What’s the investment outlook for pension funds in 2019?

Since these changes were introduced, Concordia’s plan has met all of its return targets. And the new investment strategy has been particularly effective in protecting capital in times of large market losses, says Gauthier, noting it’s also performed when the market is moving slightly in either direction.

However, he adds, the strategy hasn’t been as effective in times of significant market growth, so this will be a future area of focus for the plan.

Yaelle Gang is editor of the Canadian Investment Review.