Investors were already feeling the pressures of historically low interest rates. Then came the coronavirus pandemic.

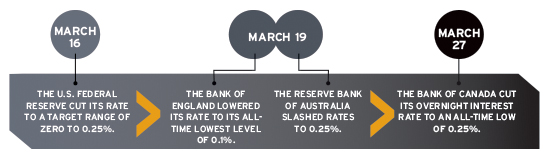

The Bank of Canada cut its overnight interest rate at the end of March to an all-time low of 0.25 per cent and announced a plan to spend $5 billion per week on Government of Canada bonds. This came 10 days after the U.S. Federal Reserve slashed interest rates to effectively zero. Around the world, many other major central banks made similar rate cuts.

And in a true sign of the times, the Bank of Nook in Nintendo Co. Ltd.’s hit video game and quarantine favourite Animal Crossing steeply reduced its interest rates paid on savings in late April, forcing gamers to speculate on turnips and tarantulas on the game’s “stalk” market.

Read: Canadian DB plan solvency drops off coronavirus scare: reports

While these emergency actions recall central banks’ tactics during the 2008/09 financial crisis, current circumstances differ in one crucial way: consumer power has taken a severe and immediate blow, forcing central banks to keep the economy afloat almost entirely on their own for the time being.

“I do believe the consumer is really the only solution to get us out of this crisis,” says Ruo Tan, president of Segal Rogerscasey Canada. “Without the consumer, no matter how much money the [central banks] will put in, it won’t sustain the economy itself.”

This, combined with the new recessionary environment, will ensure drastically low interest rates are here to stay for many years. The Fed suggested as much at the end of April when it promised to maintain its rates in the zero to 0.25 per cent range until “it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.”

Pension funds were already feeling the strain. In response to the low rate environment pre-coronavirus, many multi-employer and jointly sponsored plans announced discount rate reductions in their 2019 annual reports. The Colleges of Applied Arts and Technology pension plan cut its rate from 5.5 per cent in 2018 to 5.15 per cent for its actuarial valuation at Jan. 1, 2020.

Read: CAAT pension plan returns 16% in 2019, well-positioned to weather coronavirus storm

In its report, the Healthcare of Ontario Pension Plan said a 30 basis-point change in its discount rate, from 5.3 per cent in 2018 to five per cent in 2019, increased its liabilities and resulted in a two per cent decline to its funded ratio on a smoothed assets basis. And the Nova Scotia Teachers’ Pension Plan reduced its rate, from 6.05 per cent in 2018 to 5.7 per cent in 2019, noting the move was reflective of a “protracted lower interest rate environment and a prolonged slowdown of global economic activity.”

As for single-employer defined benefit plans, “you can’t earn your way of out this one if you’re a solvency funder,” says Janet Rabovsky, an independent investment consultant. “Obviously, [plan sponsors] have to look at their asset mix to make sure they’re still earning a decent amount in a sensible way, but the real issue is the denominator, not the numerator.”

Diversification and risk-reduction

Years of low interest rates have seen pension funds move away from fixed income in search of better returns and due to a belief that rates couldn’t drop much further, says Nathan LaPierre, a partner in retirement solutions at Aon.

“Plan sponsors that haven’t embraced liability-driven investment strategies have been thinking that for a long time, because interest rates have been low for a long time, but we see they keep going lower. That line of thinking hasn’t worked out yet.”

Read: Half of institutional investors concerned about fixed income liquidity: survey

The current environment is the clearest proof that interest rates can always be cut further, he says, urging plan sponsors to assess whether they can handle that. “If [they] can’t, yes, [they] do still need fixed income.”

With dramatic pressure on interest rates, plan sponsors are re-evaluating what type of fixed income they should own during the crisis. In the first quarter of 2020, the FTSE Canada universe bond index posted 1.6 per cent. The RBC Investor and Treasury Services universe noted investors were fleeing to safety, with the FTSE Canada high-yield index returning negative nine per cent and the FTSE Canada federal bond index out-performing its riskier peer, at 5.1 per cent.

Time to rebalance

Overweight in fixed income and underweight in equities as a result of the extreme market volatility in early March 2020, pension funds are expected to rebalance to their target asset mix in the coming quarters. JPMorgan Chase & Co. analysts said they anticipate US$400 billion will flow into the stock market as plans go about rebalancing their portfolios. However, they noted, this might be a conservative estimate — in 2009, in the aftermath of the global financial crisis, pension funds bought US$200 billion in stocks or US$600 billion in today’s dollars.

Sun Life Global Investments (Canada) Inc. was among the investors moving to high-quality bonds during the crisis to help reduce portfolio risk, says Kathrin Forrest, assistant vice-president of portfolio management at SLGI, who manages total return portfolios for defined contribution plan sponsors, including the insurer’s employee plan.

Up until recently, Canadian bonds have generated decent returns for pension funds, with the FTSE Canada universe bond index returning 4.34 per cent annualized in the 10-year period that ended March 31, 2020. “But the current interest rate levels are clearly unprecedented,” she says, noting the yield for tenure on Government of Canada bonds has fallen from more than 3.5 per cent to well under one per cent in the past 10 years.

SLGI has also diversified its bond holdings geographically, particularly to the United States where it sees more opportunities; adopted high-yielding credit with an emphasis on active credit selection; and upped its exposure to less liquid markets such as private fixed income and commercial mortgage-backed securities, seeking to capture a yield premium over publicly issued bonds.

Read: Will social bonds grow in popularity with coronavirus recovery?

“But let’s not forget, bonds have also played a role in diversifying and reducing overall portfolio risk,” says Forrest. “As we explore and implement opportunities to generate more income or enhance expected returns, we want to be mindful of the impact of overall portfolio risk, whether that’s correlations, credit, liquidity or fair valuation on an ongoing basis.”

While a move down the credit quality spectrum offers the opportunity for higher yield — and, as LaPierre notes, is one strategy often employed by pension funds in low interest rate environments — those asset classes face new challenges

in the pandemic.

“One of the interesting things during COVID-19 [is], . . . while interest rates on federal government bonds are so low, rates on corporate debt and credit risk have actually increased quite substantially,” he says. “Corporate bond yields are higher than they were before COVID-19, which is the market expecting defaults and downgrades.”

Similarly, Tan says even riskier types of government debt, such as municipal bonds, face new headwinds. “If people don’t have jobs, they can’t pay their mortgages [or] their property taxes and municipal bonds will be in trouble. The payment from municipal bondholders is simply from property tax.”

In search of yield

In a low rate environment, the first strategy for pension plan sponsors to pursue is an expansion into other assets that provide reliable income and will help offset some of the pain they’re feeling, says Wylie Tollette, head of client investment solutions in Franklin Templeton’s multi-asset solutions business. “That’s why you’re seeing many pension plans invest in commercial real estate. . . . Rental income can [be] and has been resilient in the face of lower interest rates.”

Read: 2020 Top 40 Money Managers Report: Hold your ground

A real estate asset’s capitalization rate — a valuation measure calculated as the ratio between an asset’s net operating income and its original capital cost or current market value — is connected to interest rates and will fall as they do, but not by as much, he says. “They do provide a little bit of diversification benefit. They still have a pretty good income profile, but they also come with risk. A building can be impacted by a lot of different things. It can get old and look shabby and have a hard time filling itself with tenants. It can have environmental issues or structural problems. It takes a lot more risk than buying a government bond.”

Historically, real estate has only been an option for much larger pension plans, but a proliferation in funds has opened up access to smaller plan sponsors, giving them a similar ability to diversify as the majors, says Tollette.

Absolute return vehicles like hedge funds are also popular with pension funds in low rate environments. Most absolute return strategies, which are designed to generate modest positive rates of return in almost any environment, involve tactical allocations across asset classes, short-term oriented trading strategies and take advantage of the short-term mispricing of assets. While Tollette cautions these strategies “don’t absolutely provide the return they absolutely promise,” he notes they can be a good source of return when fixed income is underperforming.

Read: What are the implications for pension funds coming out of coronavirus crisis?

“The common characteristic of absolute return is they’re not as immune from market impact as promised, but they are largely and well used by pension plans in very low interest rate environments as a substitute for fixed income that’s not providing much yield.”

In the wake of the pandemic, central banks’ aggressive moves may serve to benefit infrastructure, adds Tan. “What’s unique about this particular crisis is the announcement by the Fed to say this time that quantitative easing is without any limit. They can basically increase circulation as much as they can to increase the liquidity of the financial markets and the banking system itself. . . . If this becomes a normal circumstance, future inflation will be quite high. All that said, it will be diluted, because you have so much money in circulation; it will cause very high inflation on the real assets — the bridges, the housing market. Infrastructure will be a good investment in the future.”

The great rebalancing

With the pandemic wreaking havoc on global markets, it’s likely many pension funds have found themselves underweight on equities. Analysts from JPMorgan Chase & Co. said in late March they anticipate up to US$400 billion could flow into the stock market as plans look to rebalance to their target allocations. However, they noted, the timing of those expected flows is still unclear.

Key takeaways

• Interest rates are expected to stay drastically low for years to come as central banks work to stabilize their countries’ economies in the fallout from the coronavirus pandemic.

• While bonds have delivered increasingly lower returns, fixed income still plays an important role in the

pension portfolio, offering diversification and reducing risk.

• A popular move for pension funds in low interest rate environments is to move into riskier assets, such as commercial real estate, absolute return vehicles and infrastructure to generate higher returns.

AGS Automotive Systems is among the plan sponsors looking to rebalance. According to Winston Woo, the automotive supplier’s executive director of tax, pensions and government programs, its DB plan began reducing its weight in equities in 2019 in anticipation of a downturn, ending up with a portfolio split of 60 per cent fixed income and 40 per cent equities by the time the crisis hit.

Read: The impact of coronavirus on DB pension funding status, asset mix

“In 2019, as the equity markets rallied and were over 180 months of economic expansion, [we thought] the bull market was long in its tooth, so we became increasingly focused on capital preservation and building liquidity through 2019 and into this year,” he says. “So fortunately, it helped us navigate the very difficult conditions at this point in time.”

As part of its risk-mitigation strategy prior to the crisis, AGS went into long-term bonds and took some exposure to core-plus funds to generate a high yield that could match its liabilities. It also hired value-style asset managers to provide better downside protection in a down market. “Obviously, that’s a tradeoff, because it implies sacrificing the upside. . . . They may not be exciting plays, but they help stabilize the portfolio.”

Woo says AGS expects interest rates will stay low for years to come. To deal with that reality, the company has plans to carefully rebalance to get back to a 60 per cent equity allocation in the long term. “As we rebalance and redeploy, we’re going to have to do it very carefully and layer [equity] in to participate in any potential upside,” he says. “There seems to be a disconnect between the equity markets and the wider economy and we have to be careful about when and where we deploy.”

Kelsey Rolfe is an associate editor at Benefits Canada.