As private equity becomes a more sizeable part of Canadian pension portfolios, the British Columbia Investment Management Corp.’s resources and staffing are growing with it.

In April 2016, when Jim Pittman joined the BCI as its senior vice-president of private equity, his group comprised six or seven people. Three and a half years later, the private equity team has ballooned to 37 members, with 26 specifically focused on developing relationships within the private equity space and investing in funds and direct deals.

Read: BCI posts 6.1% return for fiscal year, driven by private assets

The organization’s allocation to private equity has also trended up, from 5.6 per cent of its portfolio in 2016 to 8.5 per cent in 2018. Between 2017 and 2018, the BCI committed more than $4.8 billion in new capital to private equity, with notable deals including its participation in an investor group that acquired payment and commerce solutions company VeriFone Systems Inc. and a co-investment to acquire custom window dressing company Springs Window Fashions, both in April 2018.

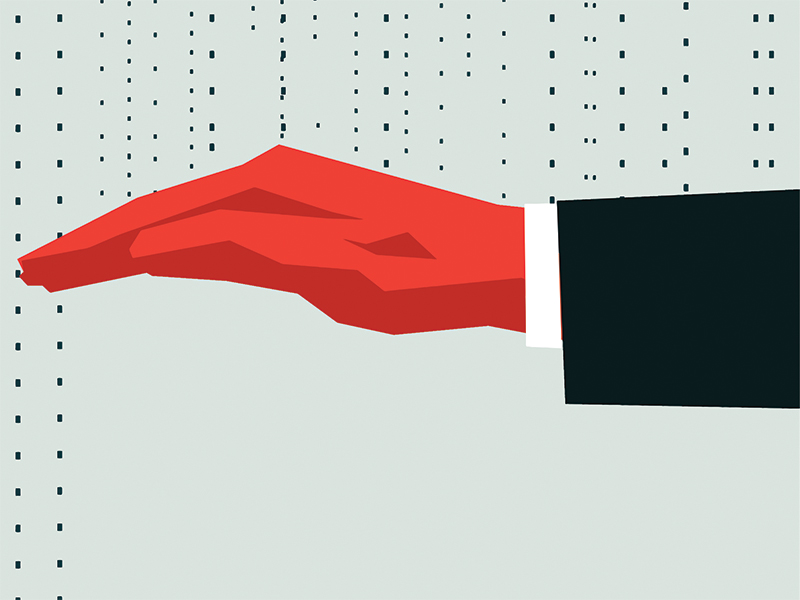

THE BCI’S PRIVATE EQUITY

BY THE NUMBERS

6-7

Team members in April 2016

37

Team members today

26

People focused on relationship-building and direct deals

5.6%

Of the BCI’s assets under management were dedicated to private equity in 2016

8.5%

Of AUM was dedicated to private equity in 2018

$4.8 billion

New capital invested in private equity in 2017-18

By comparison, its portfolio’s public equity presence is shrinking — it represented a weighty 48.3 per cent of total assets in 2017, but the proportion has dropped to 40.5 per cent in 2018.

For an organization like the BCI, both private and public equity allocations have to be considered through the lens of what its pension fund clients need, notes Pittman. “We have a number of clients, so we had to look through our client base — some clients want more [private equity] more quickly and some of them are a little bit slower, and part of that’s driven by their funding ratio. Some want to take more risks and some do not.”

A pension plan’s funded ratio is an important part of the private versus public equity conversation. While public equity’s liquidity may appeal to plans with a lower funded ratio, its volatility can present challenges. Private equity can offer more stability, but comes with the risk of locking up funds in investments for at least five to 10 years, preventing plans from cashing out if they need a liquidity infusion.

Read: The changing landscape of public and private equity investing

“We have to put all that into our crystal ball and look at how we make sure we provide our clients with the right mix of private equity and public equity,” says Pittman.

The case for private markets

The BCI is part of an ongoing shift as institutional investors — looking to improve returns, reduce volatility and diversify their portfolios — move from public to private equity. From 2006 to 2017, Canadian pension plans nearly doubled their allocations to alternative assets, starting at 15.3 per cent of investments and growing to 30.3 per cent, according to research by the Pension Investment Association of Canada.

A major factor driving institutional investors to private equity is historically low interest rates, which are depressing returns across asset classes, as well as the increasing volatility of the public markets, says Jafer Naqvi, vice-president and director of fixed income and multi-asset at TD Greystone Asset Management.

“The case for private markets . . . is institutional investors are trying to find a way to overcome this low interest-rate world with something other than taking on more risk in the stock market or higher-yielding debt,” he says. “With private markets, you can often derive an illiquidity premium for not being in the public markets.”

Read: Canadian investors standing out on alternative asset allocation: survey

While many investors believe in the illiquidity premium — that higher returns for private equity are the natural reward for locking up assets in an investment for years — some experts dispute the idea. A March 2019 report by BlackRock suggested that the stronger returns from private market investments are more tied to their complexity or higher governance costs than their illiquid nature.

Another benefit of private equity is its low volatility and stable return profile, but Naqvi says the perception that it’s less risky is largely due to how often assets are measured. “There’s a smoothing effect because you’re not following the stock market’s ups and downs. We’ve tried to remove that effect . . . to determine what is the true risk of an asset class, and when we do that we find all private asset classes have more volatility than if you measured them infrequently. Private equity, when we do that, exhibits the risks and volatilities aligned with small-cap equities.”

He also notes private equity assets can have more risk depending on how much work is involved for the investor, such as restructuring a company to improve its prospects.

Maria Pacella, portfolio manager and senior vice-president of private equity at Vancouver-based PenderFund Capital Management Ltd., says private equity increasingly makes sense for investors looking for exposure to technology sector companies with high growth potential. “You really do have to look at private markets, otherwise it’s just Netflix and Apple and Microsoft,” she says.

A September 2019 paper by Willis Towers Watson’s Thinking Ahead Institute found the global private equity industry has grown by 500 per cent since 2000. This corresponds to the trend whereby companies are raising far more capital in the private market before turning to the public sphere. As well, private deals are increasingly preferable to listing on the public markets because they offer companies longer time horizons to start generating returns and don’t have the same regulatory compliance requirements.

Read: How to benchmark performance when assets are private

“Public market investors are now accessing companies at a later stage in their development than in the past,” said Liang Yin, senior investment consultant at the Thinking Ahead Group, in a press release. “When these companies list publicly, they emerge as mature and larger companies, which can lead to public market investors missing out on significant growth opportunities and reduce the attractiveness of such investments.”

In addition, the growth in the private equity industry is reflecting a decrease in public equity markets. “Public equities, in the last 10 years, have generated nice returns,” says Karen Rode, partner in retirement solutions at Aon. “Of course, the last year has been a bit rocky, but [institutional investors are] seeking something more than that. . . . I’m not sure how much this is driving [the growth in private equity], but it’s an interesting thing that impacts the public markets — the number of public companies has dropped considerably.”

RECENT PRIVATE

EQUITY MOVES

- The Caisse de dépôt et placement du Québec committed $50 million to Quebec seed funds and made a $50-million equity investment in electric scooter share company Bird Rides Inc.

- The Canada Pension Plan Investment Board acquired a stake in European digital publisher Axel Springer in a deal worth 63 euros per share.

- The Ontario Teachers’ Pension Plan launched a venture incubator called Koru to create, test and build new digital businesses.

- The Public Sector Pension Investment Board took over Australian agribusiness Webster Ltd. for AU$854 million.

One reason for this trend is fewer companies are going or staying public, either because they’re first purchased by other firms or because they opt to go private, says Rode. “So your public market is decreasing. And anything that impacts the public market causes [institutional investors] to look elsewhere.”

In the current environment, these factors are influencing the shift to private equity, but the push in that direction can be traced back to the reaction to the 2008 financial crisis.

Read: What trends are dominating private assets for 2019?

“Everyone was in 60/40 asset mixes that were predominantly Canadian-focused and traditional assets,” says Steve Mantle, managing director of institutional sales at private equity firm Ninepoint Partners LP. “After the credit crisis, they were really disadvantaged, and when they looked at [firms] closer to the endowment model, those didn’t seem to get the drawdown that they did, and they recovered faster. That was an eye-opener for a lot of people.”

Going direct

So how are institutional investors getting exposure to private equity?

It largely breaks down by size, with major players such as the Canada Pension Plan Investment Board, the Ontario Municipal Employees Retirement System and the Caisse de dépôt et placement du Québec more commonly making direct investments.

The BCI is currently targeting a goal of 40 per cent of its private equity holdings in direct deals. In those cases, it’s typically investing for a five- to 10-year period and taking between a 30 per cent and 70 per cent ownership stake in a company. “We have a lot of governance,” says Pittman. “We know the strategies of the corporations that we’re buying. We’re heavily involved in overseeing what those are.”

The BCI isn’t alone in ramping up direct investments. A 2017 BNY Mellon survey of 350 global institutional investors found 55 per cent are looking to increase their direct investment activity.

Read: Canadian investors standing out on alternative asset allocation: survey

Another report, by CIBC Mellon in 2019, noted Canadian institutional investors are increasingly partnering up on co-investments, with 36 per cent of respondents saying their firm currently employs that investment model. Co-investments can improve the economics of investing in alternatives, the report noted, by reducing the fees paid to managers for each partner.

Funds on funds on funds

For small- and medium-sized plans, funds or funds of funds are typically the only option. A fund vehicle provides investors with exposure to a grouping of companies based on geography or industry; a fund of funds is a portfolio of investment funds. While this option makes sense for investors with less heft than the major players, Mantle notes it comes with the risk of investing in a bad “vintage,” a catchy term for the year the first major influx of capital flows into a new fund or company.

The year itself — especially if it’s at the peak or the bottom of an economic cycle — can impact the fund’s returns. “You might have a fantastic manager . . . and the first five vintages are fantastic, but this one could be terrible,” he says. “It’s the luck of the draw.”

The best way for investors to manage that risk, according to Mantle, is to diversify their vintages, by investing regularly in private equity funds.

SEISMIC SHIFT

- The private equity industry has grown 500% since 2000, according to Willis Towers Watson’s Thinking Ahead Institute.

- Between 2006 and 2017, Canadian pension plans’ allocations to alternative assets nearly doubled, from 15.3% of investments to 30.3%, according to the Pension Investment Association of Canada.

From a manager perspective, the fund allocation process is far from simple, says James Livingstone, chief executive officer at Ardenton Capital Corp. It’s a highly competitive game that requires resources to do due diligence, build relationships that will bring in good deals and make the investments themselves.

Read: Pension plans turning to alternatives for steady returns amid ultra-low bond yields

As well, he notes, geography plays a significant role. Ardenton, which purchases and holds companies for up to 25 years, allowing pension funds and other investors to invest directly into a pool of companies or through funds, invests in low- and middle-market deals of less than $100 million in Canada, the U.K. and the U.S.

“In the U.S., it’s incredibly competitive, the pricing’s really high,” says Livingstone. “In Canada and England, it’s a bit better, but for valued businesses there’s just an incredible amount of competition right now.”

However, he notes, with the return guidance for the S&P 500 sitting at around five or six per cent, and benchmark private equity returns in the U.S. at between nine and 15 per cent, it makes it worthwhile to get in the game.

Institutional investors could also see higher returns by getting involved in Asia and other international markets, which involves taking more risks, especially with ongoing recessionary headwinds, adds Livingstone. “If you’re not invested in the States, which has a positive GDP of 2.5 per cent, you have to really know your industries and the risk you’re taking. There’s not a lot of places to go that can give you growth these days.”

Read: New report tracks Canadian pension funds’ rising interest in Asia-Pacific

That’s why the BCI has balanced out its direct deals by ramping up its investments in funds, says Pittman. These funds provide exposures the organization couldn’t easily get otherwise, such as Asia, emerging markets or “specific strategies in technology or disruption — areas that, as a pension plan, we’re not fully equipped as yet. We’re building teams around those themes, but we had to be realistic about what we can invest in today.”

With just six per cent of its assets in private equity, Alberta’s Local Authorities Pension Plan still manages to use three different methods of allocation. It has taken on co-investments, direct deals and private equity funds, all directed by the Alberta Investment Management Corp., says Chris Brown, the fund’s chief executive officer.

The fund is preparing for an asset mix review next year, he adds, noting he “would not be surprised” if the LAPP decides to move further into alternatives.

Kelsey Rolfe is an associate editor at Benefits Canada.